How to Build a US Credit Score as a New Expat

Moving to the US means starting over in more ways than one: a new city, a new job, a new apartment - and a completely blank financial history. Your credit record from home does not transfer. The US credit bureaus do not communicate with international banks. Whatever you built back home, here you are essentially invisible.

That invisibility has real consequences. Without a credit score, you’ll pay bigger deposits on apartments, get worse rates on car insurance, and struggle with basic contracts like phone plans. How to build credit as an immigrant is one of the first practical problems to solve after arrival, and the earlier you start, the better. The system rewards people who begin immediately, even if their first accounts are small and simple.

Do Immigrants Have Credit Scores When They Arrive in the US?

Do immigrants have credit scores when they show up? No. You start from scratch regardless of your financial history elsewhere. Someone with a perfect repayment record in Germany or Japan arrives here with a blank slate. The US system has no way to know about it. The three main US bureaus - Equifax, Experian, and TransUnion - only track US activity.

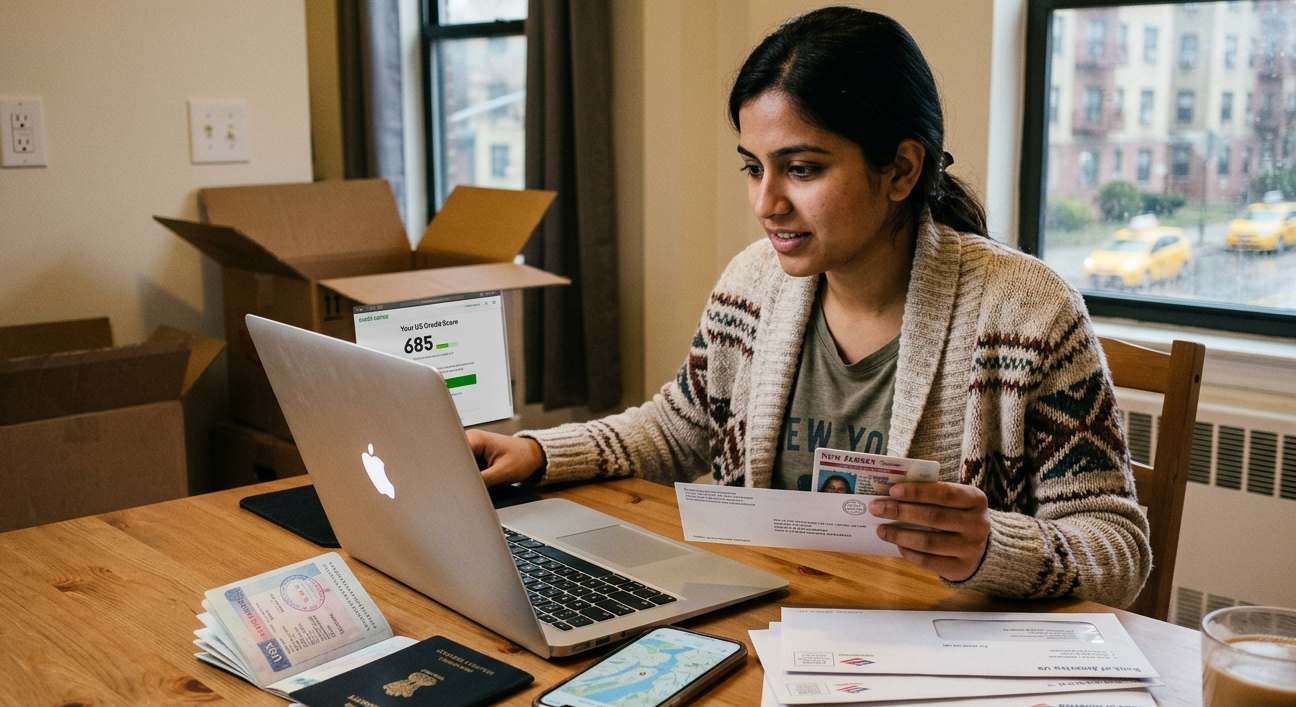

A credit score is how lenders measure whether you’re likely to pay back borrowed money. Landlords use it to screen tenants. Utility companies use it to decide whether to charge you an extra setup fee. It affects more of daily life than most people expect.

The good news: after you open your first US account and use it consistently for about 6 months, a score is generated in the system. That’s the milestone to aim for. Until then, your non-US citizen credit score simply doesn’t exist - which is why starting on day one matters.

Does Immigration Check Credit History During the Visa Process?

A lot of people worry about this one. Does immigration check credit history when reviewing visa applications or green card petitions? For most standard processes, no. USCIS doesn’t pull your credit report as part of the review.

Does immigration check credit history at all? The focus is on financial stability, not your FICO score. Officers want to ensure you won’t rely on government assistance - what’s called becoming a “public charge.” For that, they look at income, assets, and your sponsor’s financial standing. Bank statements and tax returns are relevant. Your credit score isn’t.

That said, keeping your finances organized is smart. Significant unexplained debts or financial chaos can raise questions in high-stakes interviews. Going into any immigration interview with clear records of your savings and incoming US income is the right approach. But you don’t need to worry that a thin credit file will hurt your visa outcome.

Can You Build Credit with an ITIN Number?

Not everyone arriving in the US is eligible to receive a Social Security Number immediately. Spouses of certain visa holders, students, and some foreign investors often need to wait. If that’s your situation, you can apply for an Individual Taxpayer Identification Number - an ITIN - from the IRS.

Can you build credit with an ITIN number? Yes. Many banks and credit card issuers accept an ITIN in place of an SSN. The bureaus track your activity under your ITIN the same way they would track it under an SSN. Good payment history is good payment history regardless of which number it’s filed under.

To get started, apply for the ITIN through the IRS. It typically requires filing a federal tax return or proving you’re exempt. The process takes a few weeks, but it’s straightforward. Once you have the nine-digit number, look for ITIN-friendly financial institutions - many major banks and local credit unions will work with you.

If you eventually receive an SSN, you can often merge your ITIN history into the new profile so you don’t lose the progress you’ve made.

Best Immigrant Credit Cards to Start Building US Credit

Without a US credit history, most standard rewards cards will reject you. The right starting point is a secured credit card. You put down a deposit - typically $200 to $500 - which becomes your credit limit. Because the bank carries no real risk, approval rates are very high.

Fintech companies and neobanks have also created cards specifically for new arrivals. These often evaluate you based on your bank account balance or an employment offer letter rather than requiring a credit score. They exist precisely for this situation.

When comparing immigrant credit card options, look for:

- No annual fee. You want a card you can keep open indefinitely. Closing your oldest account damages your credit age.

- Reports to all three bureaus. Not all cards do this. A card that only reports to one bureau gives you incomplete coverage.

- Path to unsecured. The best secured cards will return your deposit after 6 to 12 months of consistent on-time payments and automatically upgrade you.

Once you have a card, use it for small recurring purchases - a streaming subscription, regular groceries - and pay it off completely every month. Don’t carry a balance. The goal is to demonstrate reliability, not to borrow money.

How to Build Credit as an Immigrant: Step-by-Step

How to build credit with an ITIN or an SSN follows the same basic path. Here’s the process:

- Open a US bank account. This is usually the first step. A banking relationship with a US institution makes credit applications easier and establishes your presence in the system.

- Apply for a secured or starter card. Use whatever number you have - SSN or ITIN - to apply for a card that reports to all three bureaus. Don’t apply for multiple cards at once. Each application triggers a hard inquiry, which slightly lowers your score.

- Set up autopay. Set payments to “full statement balance” so you never carry a balance and never miss a due date. One missed payment on a thin file causes significant damage.

- Watch your utilization. Try to keep your balance below 30% of your credit limit at the time your statement closes. If your limit is $500, aim to keep less than $150 on the card when the statement is generated.

- Let time pass. The age of your accounts matters. Since everything will be new, you simply need to keep accounts open and let the months accumulate. Within 6 to 10 months of consistent behavior, you should have a functional score that opens doors to better cards and loans.

This is the core of how to build credit as an immigrant - patience combined with consistent, low-key usage.

Additional Ways Immigrants Can Build Credit in the US

Credit cards are the most common path, but they’re not the only one:

- Credit-builder loans. Some banks and credit unions offer loans in which the funds are deposited into a locked savings account while you make monthly payments. Once the loan is paid off, you get the funds - and you’ve built a year of on-time payment history. These are specifically designed for people with no credit, and the approval process doesn’t depend on an existing score. The amounts are usually small ($300 to $1,000), but the impact on your history is real.

- Becoming an authorized user. If you have a friend or family member in the US with a long credit history, being added as an authorized user on their account can partially boost your own profile. Their account history shows on your report. You don’t even need to use the card. Just being associated with an account that has years of good history adds something to yours. Choose carefully, though. Their missed payments would also show up on your report, so this only works if the primary cardholder is reliably responsible.

- Rent and utility reporting services. Standard rent payments don’t appear on credit reports. But several services will report your rent to the bureaus if you opt in. For a new arrival paying rent each month, this is a simple way to build history that would otherwise not count.

- International credit transfer services. Companies like Nova Credit work with some US lenders to translate your foreign credit history into a format American lenders can read. If you’re from India, Mexico, the UK, Australia, or several other countries, your history back home can help you get a quality immigrant credit card or loan upon arrival, rather than starting from scratch.

This last option is one of the fastest approaches to how to build credit as an immigrant - it lets you use the work you already did.

Returning to the question: Does immigration check credit history as a formal part of the visa or green card process? The standard answer is no. But the broader principle matters - keep your US finances clean and organized regardless. A good non-US citizen credit score helps you in everyday life, not in immigration offices.

Common Mistakes to Avoid When Building Credit as a Non-Citizen

Building a non-US citizen credit score from nothing takes time. However, people often make mistakes due to a lack of knowledge or experience. That’s why we’re here to help you avoid them:

- Applying for too many cards at once. Every credit application results in a hard inquiry on your credit file. Applying for multiple cards in a short period signals financial desperation to lenders. Pick one card, get established, then wait at least six months before considering another application. A single rejection doesn’t mean you should immediately try somewhere else. It usually means you need to build more history first.

- Closing your first account. Your first card is the foundation of your credit age. Even if you get a better card later, keep the original one open. Closing it shortens your history and can reduce your available credit, both of which hurt your score.

- Ignoring utilization timing. Even if you pay off your balance every month, the balance reported to the bureaus is the amount on the date your statement closes, not after you pay. If you have spent $450 on a $500 limit card, pay it down before the statement date, not after. This is one of the most common mistakes people make, even though they are otherwise doing everything right. The timing of the payment matters as much as whether you pay at all.

- Co-signing for someone else. Your early credit profile is fragile. If someone you co-sign for misses payments, it affects your score just as much as theirs. Hold off on that until your file is more established. Even one or two years of good history makes a significant difference in how much damage you can absorb from someone else’s mistakes.

The system rewards consistency and penalizes impulsiveness. Follow the steps, avoid the traps, and by the end of your first year, you’ll have a functional score that reflects well on the financial life you’re building here. By the second year, you’ll likely qualify for better cards, real loans, and the kind of financial flexibility that makes everything else easier.

Expat-US helps people navigate the full relocation process, including the financial steps that aren’t always obvious when you first arrive. Contact us for guidance on settling in effectively.